Are Electric Cars More Expensive to Insure?

Electric cars are getting more affordable. Charging is cheaper than filling up. Servicing costs less. However, one question keeps coming up: what about insurance?

It's a fair concern. EV insurance premiums have been higher than petrol and diesel equivalents… and if you've ever searched for a quote on a Tesla or a BMW iX, you'll know the numbers can raise an eyebrow or two.

But the gap between EVs and traditional cars is closing faster than most people realise, and - as we'll cover later - there's one route to getting an electric car where insurance isn't something you need to think about at all.

Here's everything you need to know.

What is the cost of insurance for electric cars?

It depends on the car.

Electric car insurance in the UK can range anywhere from around £400 to well over £1,000 a year. The median comprehensive EV policy cost £572 in late 2024, according to GoCompare. But that average masks a pretty wide spread.

Here are a few examples of real-world examples:

- Smaller EVs like the VW ID.3, Mini Cooper Electric, and Nissan Leaf can start from just over £400 a year for drivers with a clean licence

- Step up to a Tesla Model 3 and you're looking at closer to £900

- Go premium (think Mercedes EQC or a high-spec Tesla) and £1,000+ is considered ‘reasonable’

So before you panic, it's worth asking: which electric cars are we actually talking about?

How do EV insurance costs compare to Petrol and Diesel cars?

Yes, EVs are more expensive to insure than petrol and diesel cars right now. But, the gap is smaller than you might think, and is closing fast.

At the start of 2024, the median comprehensive EV policy cost £623, compared to £447 for a standard car - a difference of £176.

Since then, EV premiums have been falling faster than petrol and diesel equivalents, and that trend is expected to continue.

So why the gap at all? A few reasons insurers will give you:

- Battery costs. The average cost of a new EV battery across all models was £7,235 in 2024 (and that doesn't include labour). When a battery gets damaged in even a minor accident, that bill lands on the insurer.

- Specialist repairs. Not every garage can work on an EV. High-voltage systems require specific qualifications, which means fewer available technicians and higher labour rates when you do find one.

- Repair costs overall. According to automotive data company Solera, repair costs for EVs are up to 29% higher than for petrol and diesel cars.

- Higher vehicle values. Pricier cars cost more to replace when written off, and many EVs still sit at the premium end of the market.

Most of these factors are temporary.

As EVs become mainstream, repair networks are growing, insurers are accumulating claims data, and premiums are responding accordingly.

It's also worth zooming out. Insurance is one line item in the total cost of running a car. The RAC found that in November 2025, charging an EV at home cost around 8p per mile. That’s roughly half the cost of petrol or diesel at 15–16p per mile.

Factor that in alongside lower servicing costs, and the full picture looks quite different from the headline insurance figure.

There’s one more thing worth knowing:

The running costs that sit alongside your insurance premium, like charging, servicing, and tyres, are all significantly lower for EVs than most people expect.

Take a look at how much it actually costs to charge an electric car in the UK if you want the full picture before making a decision.

And check out how petrol cars compare to EVs to get a side-by-side look at the purchase running costs.

How is car insurance calculated? (And why EVs score differently)

Car insurance works the same way whether you're driving a petrol Fiesta or an electric Polestar. Insurers are pricing risk.

According to the ABI, the cost of your premium is essentially the insurer's estimate of how likely you are to make a claim, with the premiums of the many covering the claims of the few.

The standard factors apply across all cars:

- Your age and experience: younger drivers pay more, premiums generally fall after 25

- Your driving history: convictions and past claims push prices up

- Where you live: urban postcodes with higher theft and accident rates cost more

- Annual mileage: more miles driven means more exposure to risk

- Your voluntary excess: agreeing to pay more upfront in a claim can bring your premium down

But EVs introduce a few extra variables on top of all of that. Every car is assigned to an insurance group from 1 to 50, based on factors like vehicle value, the cost and availability of parts, repair times, performance, and security features. EVs (especially newer models) tend to cluster toward the higher end of that scale.

There are three EV-specific factors that matter most to your premium:

- Battery value. It's the most expensive component in the car and often the first thing affected in a collision. Insurers price that risk in.

- Specialist repair requirements. High-voltage systems need qualified technicians. Fewer of them means slower repairs and higher labour costs.

- Limited historical data. Insurers price based on past claims behaviour. EVs are still relatively new, so that data is thinner - and uncertainty costs you more.

The type of EV you choose matters as much as anything else. A used Nissan Leaf sits in a very different insurance group to a brand new Tesla Model Y and your premium will reflect that.

5 ways to reduce your EV insurance costs

There's plenty you can do to bring the cost down.

1. Shop around; look for EV-specialist insurers

Don't just auto-renew or sign up the first insurance provider you see.

Admiral shares that there's a huge range in EV premiums even within the same vehicle category, so comparing quotes can make a genuine difference.

Mainstream insurers are increasingly competitive on EVs, but specialist providers sometimes offer better value, particularly for comprehensive cover that includes battery protection and charging equipment.

2. Increase your voluntary excess

Agreeing to pay a higher excess can bring your premium down. You’ll just want to make sure it's an amount you could comfortably cover if you needed to make a claim.

It's a pretty simple lever that's easy to overlook at renewal time.

3. Install a dashcam

Have you seen all those Instagram reels and TikToks captured from a stationary camera on the dashboard of a car? Those are dashcams. Drivers use them so that they have proof if someone cuts you off and causes an accident on the M25 or if someone fakes an accident and tries to commit insurance fraud.

But even if those incidents don’t occur, having one demonstrates to insurers that you're a careful, accountable driver. Many will factor this in when calculating your quote. Just give them a heads up when getting a quote.

4. Secure your parking

Storing your EV in a locked garage rather than on the street reduces the risk of theft and can bring your insurance costs down.

If you don't have a garage, even a driveway is preferable to a public road in the eyes of most insurers.

5. Consider a telematics (black box) policy

If you're a low-mileage or demonstrably safe driver, a telematics policy can work in your favour. Insurers track how you drive and may reduce your premium at renewal if you've built up a good record.

It's particularly worth considering if you mostly use your EV for commuting and the school run rather than long motorway miles.

The better way: get insurance included with EV salary sacrifice

Here's something most people don't know when they're shopping around for EV insurance: if you get your car through a salary sacrifice car scheme, insurance is already included.

With loveelectric, fully comprehensive insurance is bundled into your single monthly payment. That’s alongside:

- Servicing

- Maintenance

- Breakdown Cover

- Tyres

No separate policies. No annual renewal to tackle. Just one simple monthly cost.

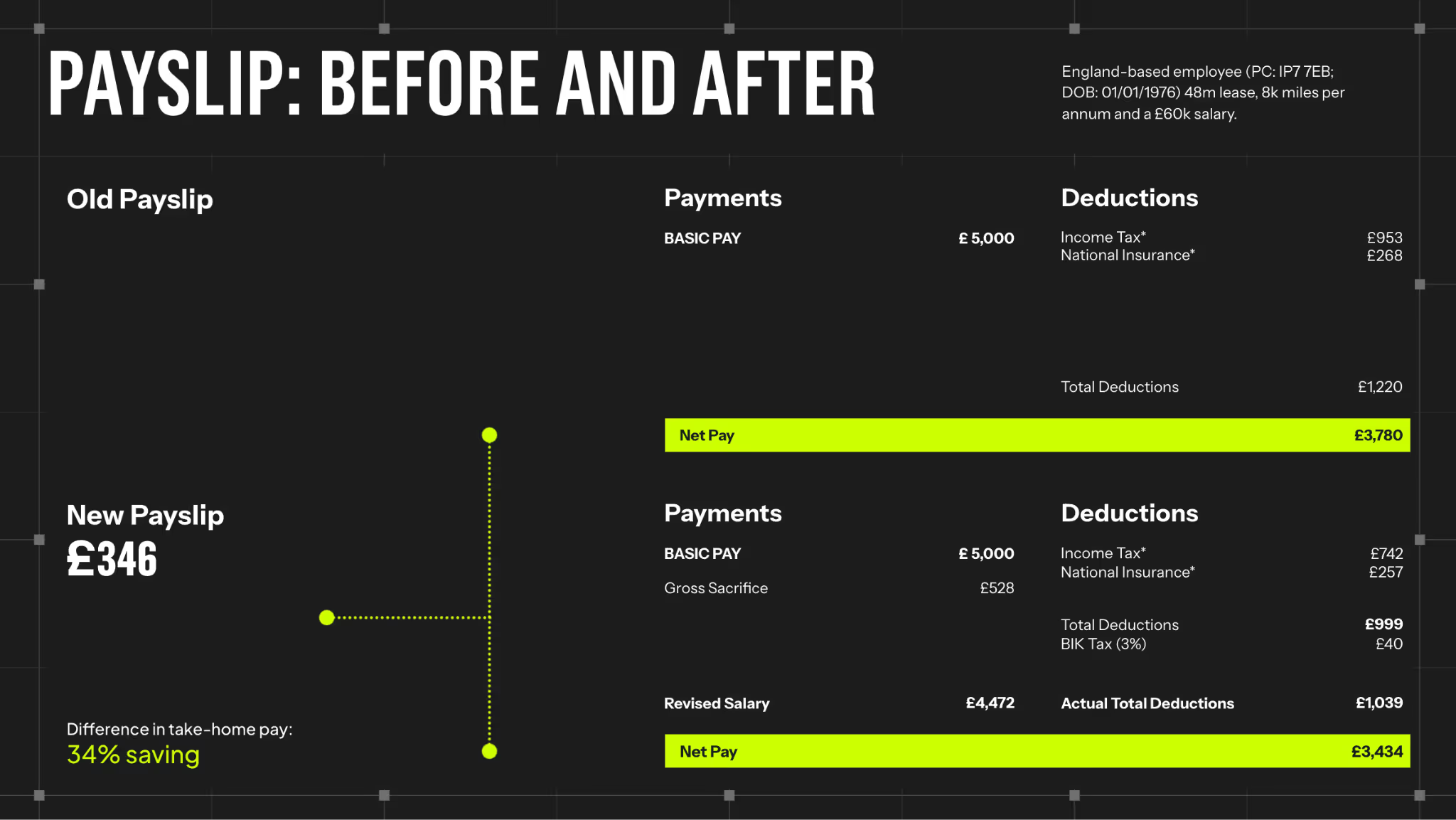

But the bigger story is what salary sacrifice does to that cost overall. Your monthly payment comes straight from your gross salary, before Income Tax and National Insurance are calculated.

So a £528/month package doesn't actually cost you £528. For a basic rate taxpayer, the real figure after tax savings is closer to £346/month. For higher earners, the savings go even further.

Take a look at a real salary sacrifice electric car example to see exactly how the numbers stack up or browse salary sacrifice electric cars to see what's available right now. We offer both new and used to cover every budget.

Not sure if the savings make sense for your salary? Our guide to employee tax benefits for EV schemes breaks it down by earnings bracket.

Ready to get started? If your employer isn't on the scheme yet, that's an easy fix. Refer your company to loveelectric and we'll take it from there.

FAQs

Why are electric cars so expensive to insure?

EVs are more expensive to repair than petrol and diesel cars. Batteries are costly to replace, specialist technicians are still in short supply, and insurers are working with less historical claims data than they have for traditional vehicles.

All of that uncertainty gets priced into your premium

Will EV insurance costs come down?

Yes, and they already are. EV premiums have been falling faster than petrol and diesel equivalents since their 2024 peak, and the gap is expected to keep closing as more electric cars hit UK roads. The direction of travel is firmly downward.

Does salary sacrifice include car insurance?

Yes, with loveelectric, fully comprehensive insurance is bundled into your monthly salary sacrifice payment alongside servicing, maintenance, breakdown cover, and tyre replacement. You don't arrange it separately or deal with annual insurance renewals. It's all included from day one. If you're new to how the scheme works, our guide to how salary sacrifice works for car schemes is a good place to start.

Is salary sacrifice worth it for an electric car?

For most employees, yes. Significantly so. The tax and National Insurance savings mean you're paying for the car from your gross salary, which brings the effective monthly cost down considerably compared to a personal lease.

The savings are biggest for higher earners, but even basic rate taxpayers typically see 30–40% off the equivalent retail price. The full breakdown can be found here: is EV salary sacrifice worth it?

Which is the best salary sacrifice car scheme?

Not all salary sacrifice providers are the same. Coverage, risk protection, vehicle choice, and pricing models vary quite a bit. We've put together a comparison of the best salary sacrifice car scheme providers to help you understand what to look for and how loveelectric stacks up.

Is EV insurance cheaper if I charge at home?

Not directly. Your charging habits aren't a standard rating factor. But home charging does reduce your overall running costs considerably. Take a look at how much it costs to charge an electric car in the UK to see the numbers.

Does my electric car insurance cover battery damage?

Usually. But be sure to check the small print. Most comprehensive policies cover the battery for accidental damage, fire and theft, whether you own or lease it.

What they typically won't cover is gradual degradation or mechanical failure. That's a warranty issue, not an insurance one.