9 Salary Sacrifice Electric Car Examples: With EV Calculator

.avif)

When searching for information on salary sacrifice electric car schemes, you might have noticed there aren't many real-world examples online showing which electric cars you could be driving and the cost breakdown of those models. There are, however, many articles explaining salary sacrifice schemes generally.

But you want specifics. You want to picture yourself in your dream EV and figure out what you really stand to save based on your salary.

In this article, we aim to clarify the confusion and get you real answers—showcasing electric cars that are available through our salary sacrifice scheme with tangible breakdowns of what the car will cost you based on your salary range and how much that car will reduce your tax.

We’ll be covering the following salary sacrifice car examples:

- 3 cars someone in the lower tax (20%) bracket can drive (with savings calculated)

- 3 cars someone in the higher tax (40%) bracket can drive (with savings calculated)

- 3 cars someone in the highest tax (45%) bracket can drive (with savings calculated)

We’ll also point you toward our nifty salary sacrifice savings calculator which is free to use and doesn’t require your email. Plus go through the cost difference in leasing vs salary sacrifice, combustion vs EVs through salary sacrifice, and an example of an order form.

Looking for a low-risk way to get started with a salary sacrifice scheme and have someone help you through the whole process? Go ahead and sign up to loveelectric for free.

Electric Car Examples from loveelectric Customers

Alexander | Mercedes-Benz EQB

What have been the key benefits of driving an electric car?

The costs are definitely reduced, our monthly costs but also the cost to fully charge the car are better especially with the increased energy costs due to the global political situation. The environmental benefits are a good point especially when being stuck in traffic in London.

Would you recommend getting an electric car through loveelectric's EV salary sacrifice scheme?

I would definitely recommend the scheme, it provides great value for money and it's very simple and straightforward.

Alex | Polestar 3

What have been the key benefits of driving an electric car?

The economics. It costs me 10% of the monthly fuel costs compared to when I had an ICE vehicle. The maintenance costs are also lower. I also enjoy that I never have to go to a petrol station during the week, my car always leaves home with a 'full tank'. Lastly, the quietness of the car is something I actually prefer.

Would you recommend getting an electric car through loveelectric's EV salary sacrifice scheme?

100% - an EV with no upfront payment, one monthly cost for all car-related expenses (insurance, tax, maintenance, servicing, and the car), and reducing my tax bill whilst getting all of the above. The ordering process was also very smooth and there are a wide range of cars available - used and new, expensive and moderate.

9 Salary sacrifice car scheme examples

At loveelectric, we’re specialists in setting up electric car salary sacrifice schemes.

We work as a broker, allowing us to get the best rates on the market, and we’re also a full-service provider, which means we help you set up the scheme, answer employees’ questions and take care of payroll and all the admin required.

You can learn more about our story here: Electric Cars are Expensive. Here’s How We’re Democratising Electric Vehicle Access At loveelectric

Over the next several sections, we’ll outline 9 salary sacrifice examples based on our offers at loveelectric.

Please note: Prices are correct at time of publication. Specific prices may fluctuate due to manufacturers' pricing, but the calculation in savings will remain the same.

Salary sacrifice car examples for a £30,000 to £50,270 salary [20% tax bracket]

If your salary falls between £30,000 and £50,270, you’re in the UK’s basic income tax bracket, meaning you pay 20% in Income Tax and 12% in National Insurance on most of your earnings.

With salary sacrifice, your car payments are deducted before those taxes are applied. In practice, that means every pound you “sacrifice” for your car costs you far less in take-home pay. (If you’re interested in the nitty gritty details, check out our article on how salary sacrifice car scheme works.)

Let’s look at what that really means in action for three popular EVs that are realistic for this salary bracket.

Please note: To make these examples easy to follow, we’ve used a few of the same cars across different salaries, such as the Fiat 500 and BMW iX, to clearly show how salary sacrifice savings scale across tax brackets. You’ll also see a range of other popular EVs available through loveelectric, showcasing what’s realistic for different budgets and lifestyles.

Example 1: Fiat 500

Let’s go through a salary sacrifice car example for an employee named Simon. Simon is on a £40,000/year salary, which would put him in the 20% tax bracket. He’s using a typical lease example of 48 months and 5,000 annual miles for the popular all-electric Fiat 500.

Below you can see the before and after of what this saving will look like on Simon’s payslip, demonstrating clearly where the savings come from. The example is from a salary sacrifice scheme with loveelectric.

Simon’s electric car lease quote from loveelectric is (gross sacrifice amount) £366 per month.

With the salary sacrifice scheme, the net cost to Simon is £255 per month.

The difference in net pay is £255, which is effectively the price that Simon will pay to lease a brand new electric car. In his case, he’s received a 30% discount on the standard lease price.

Although the lease costs £366 per month, he’ll only see a net cost of £255 from his salary since the lease is paid before tax.

Is the Fiat 500 not for you? Check out our full range of cars here or keep scrolling to see eight more salary sacrifice electric car examples.

Want to see your exact saving?

These examples are based on typical scenarios. Your saving depends on your salary, tax bracket, and the car you choose. Use our salary sacrifice calculator to see your personalised monthly cost in under 60 seconds.

→ Try the Salary Sacrifice Calculator

Example 2: Tesla Model 3 Saloon

Now let’s look at another real-world salary sacrifice car example, this time for an employee named Amira.

Amira earns £45,000 per year, putting her comfortably within the 20% tax bracket. She’s always admired Tesla’s sleek design and cutting-edge technology, so she decides to lease a Tesla Model 3 through her company’s salary sacrifice scheme.

Amira’s lease term is 48 months with an annual mileage of 5,000 miles, a realistic choice for a daily commuter with regular weekend trips.

Her Tesla Model 3 lease quote from loveelectric is a gross salary sacrifice of £602 per month.

Once tax savings are applied, her take-home pay only reduces by £453 per month. That means Amira saves around 25% compared to leasing the same car privately.

In other words, Amira’s Tesla Model 3 feels like a premium upgrade, but with a cost that fits comfortably within her monthly budget.

Although the lease technically costs £602 per month, the pre-tax structure of salary sacrifice means Amira only pays £453 in real terms. That’s a £149 monthly saving for a brand-new Tesla, proof that even premium EVs become attainable with salary sacrifice.

Safe to say for Amira, salary sacrifice is worth it.

Example 3: BMW iX Estate

Next, let’s look at an example for an employee named Jamie, who earns £50,000 per year.

Jamie’s looking for a premium SUV with plenty of space for family trips. He wants something that blends comfort, performance, and sustainability. The BMW iX Estate fits the bill perfectly.

Through loveelectric’s salary sacrifice scheme, Jamie chooses a 48-month lease with 5,000 annual miles.

His BMW iX lease comes to a gross salary sacrifice of £1,049 per month. Now, that’s pretty steep for someone earning £50k. Luckily, salary sacrifice makes it affordable.

Once Jamie’s tax and National Insurance savings are applied, his take-home pay only reduces by £657 per month, a 38% saving compared to a standard personal lease.

Although the lease technically costs £1,049 each month, Jamie only feels a £657 impact on his salary. That’s a £392 monthly saving, giving him access to a luxury electric SUV at a far more manageable cost. If he has a partner or spouse, they can be added to the insurance and split the cost of the vehicle personally (but not through the scheme itself).

That dream car is now a reality. That’s what makes loveelectric one of the best salary sacrifice car scheme providers.

Salary sacrifice car examples for a £50,271 to £125,140 salary [40% tax bracket]

If your income falls between £50,271 and £125,140, you’re in the UK’s higher-rate tax bracket, meaning you pay 40% Income Tax and 2% National Insurance on most of your earnings. That higher tax rate actually works in your favour when it comes to salary sacrifice employee benefits, because the more tax you normally pay, the more you stand to save.

For higher-rate earners, a salary sacrifice car scheme can reduce the real-world cost of driving a new EV by 40–60% compared to a standard lease. It’s one of the most effective ways to turn a premium electric car into a tax-efficient, affordable benefit.

Let’s take a look at how those savings play out with a few examples.

Example 4: Fiat 500

For this example, we’ll pick another employee called Jenifer and see what her payslip calculations look like for the Fiat 500 from our first salary sacrifice car example but on a £100,000/year salary. This puts her in the higher 40% tax bracket.

Again, Jenifer has a typical lease example of 48 months and 5,000 annual miles for the electric Fiat 500.

The salary sacrifice car scheme example quote Jenifer got on the loveelectric site for the standard lease price (gross sacrifice amount) is also £366 per month.

But through tax savings, the net cost to Jenifer is £217 per month. Because of her higher salary, she’s saving up to 40% on the standard lease price.

Looking at the table below, you get a clearer picture of the overall savings. The table shows how the 40% tax bracket benefits from even more savings than the 20% tax bracket, with £1,824 saved throughout the 48-month lease.

We can clearly see that employees in the 40% tax bracket are paying more tax and are therefore saving more compared to those in the 20% tax bracket.

Example 5: Polestar 4 Estate

For this example, let’s look at Isaac, who earns £90,000 per year, placing him within the 40% income tax bracket. Isaac wants a premium EV that balances cutting-edge design with everyday practicality — something that feels exciting to drive yet smart from a financial standpoint. The Polestar 4 Estate is a perfect fit.

Through loveelectric’s salary sacrifice scheme, Isaac has chosen a 48-month lease with 5,000 annual miles.

His Polestar 4 lease quote shows a gross salary deduction of £706 per month.

After his tax savings are applied, the real reduction to his take-home pay is just £442 per month, giving him a 38% saving compared to the standard lease price.

Although the Polestar 4 lease technically costs £706 per month, Isaac effectively pays only £442 thanks to salary sacrifice, saving £264 every month. Over a 48-month lease, that’s more than £12,600 saved on a sleek, high-performance EV that makes financial and environmental sense.

Example 6: Mercedes-Benz EQS

Finally, let’s look at Sophie, who earns £105,000 per year, placing her above the £100,000 threshold where the Personal Allowance begins to taper off. This means that for every £2 Sophie earns over £100,000, she loses £1 of her tax-free allowance, creating an effective tax rate of roughly 60% on part of her income.

To make her money work smarter, Sophie decides to get a Mercedes-Benz EQS through her company’s salary sacrifice scheme with loveelectric. It’s a luxury all-electric saloon that combines comfort, technology, and sustainability. It’s the ideal upgrade for someone who spends plenty of time on the road.

Sophie’s chosen a 48-month lease with 8,000 annual miles. Her loveelectric quote shows a gross salary deduction of £1,032 per month.

Once her tax and National Insurance savings are applied, the actual reduction to her take-home pay is just £566 per month, a 46% saving compared to a standard lease.

By sacrificing part of her pre-tax salary, Sophie not only reduces her monthly car cost from £1,032 to £566, but also brings her taxable income below £100,000, restoring her full Personal Allowance and saving even more in Income Tax overall.

In total, Sophie saves £466 per month and thousands more annually thanks to the dual benefit of salary sacrifice: affordable access to a luxury EV and smarter tax efficiency.

Addicted to the tax benefits of salary sacrifice? Learn all about them in our article: Employee tax benefits for EV schemes: How salary sacrifice with loveelectric saves you thousands

And it’s not just employees who benefit. Businesses do too. Learn how salary sacrifice supports corporate tax efficiency and sustainability in our article: Electric car company tax benefits: why EVs make financial sense for UK businesses.

Salary sacrifice car examples for a £125,140 or above salary [45% tax bracket]

If you earn over £125,140, you fall into the UK’s additional-rate tax bracket, paying 45% Income Tax and 2% National Insurance on what you earn above that figure. At this level, salary sacrifice becomes one of the most powerful and often underused ways to reduce your tax burden while accessing high-end electric vehicles at a fraction of their usual cost.

Because deductions are made before tax, higher earners can save up to 60% on the cost of an EV compared to personal leasing or purchase. In other words, salary sacrifice doesn’t just make luxury electric cars more affordable, it also makes them one of the most tax-efficient employee benefits available.

Let’s look at a few examples of how the scheme works for additional-rate taxpayers.

Example 7: BMW iX Estate

For our final BMW iX example, let’s look at Ravi, who earns £140,000 per year, placing him firmly in the 45% additional-rate tax bracket. Like Jamie in our earlier example, Ravi’s chosen the BMW iX Estate, a luxurious, all-electric SUV that blends comfort, cutting-edge tech, and long-range practicality.

Ravi’s selected a 48-month lease with 5,000 annual miles through loveelectric’s salary sacrifice scheme. His lease quote shows a gross salary deduction of £1,049 per month.

After applying his tax and National Insurance savings, the actual reduction to his take-home pay is just £615 per month, a 42% saving compared to a standard lease.

Although the BMW iX technically costs £1,049 per month, Ravi effectively pays only £615 thanks to salary sacrifice. That’s a monthly saving of £434, adding up to more than £20,800 saved across a four-year lease.

Compared to Jamie’s 20% tax bracket example, Ravi saves nearly £1,100 more each year on the exact same car. That’s a powerful illustration of how salary sacrifice benefits increase with income.

Example 8: Polestar 4 Estate

To show how savings continue to increase for additional-rate taxpayers, let’s revisit the Polestar 4 Estate, the same car Daniel leased in our 40% tax bracket example. This time, we’ll look at Priya, who earns £130,000 per year, placing her within the 45% income tax bracket.

Priya has chosen the same 48-month lease with 5,000 annual miles through loveelectric’s salary sacrifice scheme.

Her Polestar 4 quote shows a gross salary deduction of £706 per month. After her higher-rate tax savings are applied, the actual reduction to her take-home pay is just £362 per month, an impressive 49% saving compared to the standard lease price.

Although the Polestar 4 technically costs £706 per month, Priya only sees a £362 reduction in her take-home pay. That’s a saving of £344 per month, or over £16,000 across a four-year lease, a substantial gain that demonstrates just how powerful salary sacrifice can be for additional-rate taxpayers.

By comparing Daniel’s and Priya’s examples side by side, it’s clear that as income (and tax rate) increases, the savings scale up dramatically.

Example 9: Porsche Taycan Saloon

For our final example, let’s look at James, who earns £200,000 per year, placing him well within the 45% additional-rate tax bracket. As a long-time EV enthusiast, James has his sights set on something truly premium, the Porsche Taycan Saloon, a high-performance electric sports saloon that combines speed, range, and unmistakable design.

Through loveelectric’s salary sacrifice scheme, James selects a 48-month lease with 5,000 annual miles.

His Taycan lease quote shows a gross salary deduction of £1,506 per month.

However, after applying his tax and National Insurance savings, the actual reduction to his take-home pay is just £859 per month, giving him a 43% saving compared to a standard lease.

Although the Porsche Taycan lease costs £1,506 per month, James effectively pays only £859 thanks to salary sacrifice. He’s saving £647 every month, or more than £31,000 over the course of his lease.

Even for high earners like James, salary sacrifice offers a smart way to make luxury EVs more cost-effective, combining performance and prestige with genuine financial efficiency.

Staff story: Johannes, our Head of Ops

Making sense of your salary sacrifice savings

Across every tax bracket, one thing’s clear, salary sacrifice scales beautifully. The higher your tax rate, the greater your savings, but every earner benefits from paying for their car before tax.

Whether you’re a first-time EV driver saving on a compact model or a high-income professional choosing a premium electric saloon, the outcome is the same: a brand-new electric car for far less than you’d pay through a standard lease.

If you’re ready to take the next step, our How to Get a Car on Salary Sacrifice: Step-by-Step Guide walks you through the full process. Or, if you’re wondering what happens after your lease ends, our article Can You Buy a Car with Salary Sacrifice? Your Options explains whether you can transition from leasing to ownership.

Now that we’ve seen how salary sacrifice impacts different earners, let’s put it into context. How do these savings stack up against a traditional lease?

Comparing PCP vs salary sacrifice (with an example)

A PCP (personal contract purchase) is one of the most common ways to get an electric car, so it makes sense to compare it with a salary sacrifice scheme.

People like PCP as they are cheaper than taking out a loan to buy a car outright. It also offers flexibility in the way you have different options at the end of your contract, including buying the car or trading it in.

There are a few things to note when comparing PCP to salary sacrifice. The first is that maintenance and insurance are not included in a PCP. Also, if you go down the PCP route, be prepared to pay the upfront cost of a deposit.

.avif)

You can read this in more detail here: Electric Car Monthly Cost: How Much Does it Cost to Run an Electric Car?

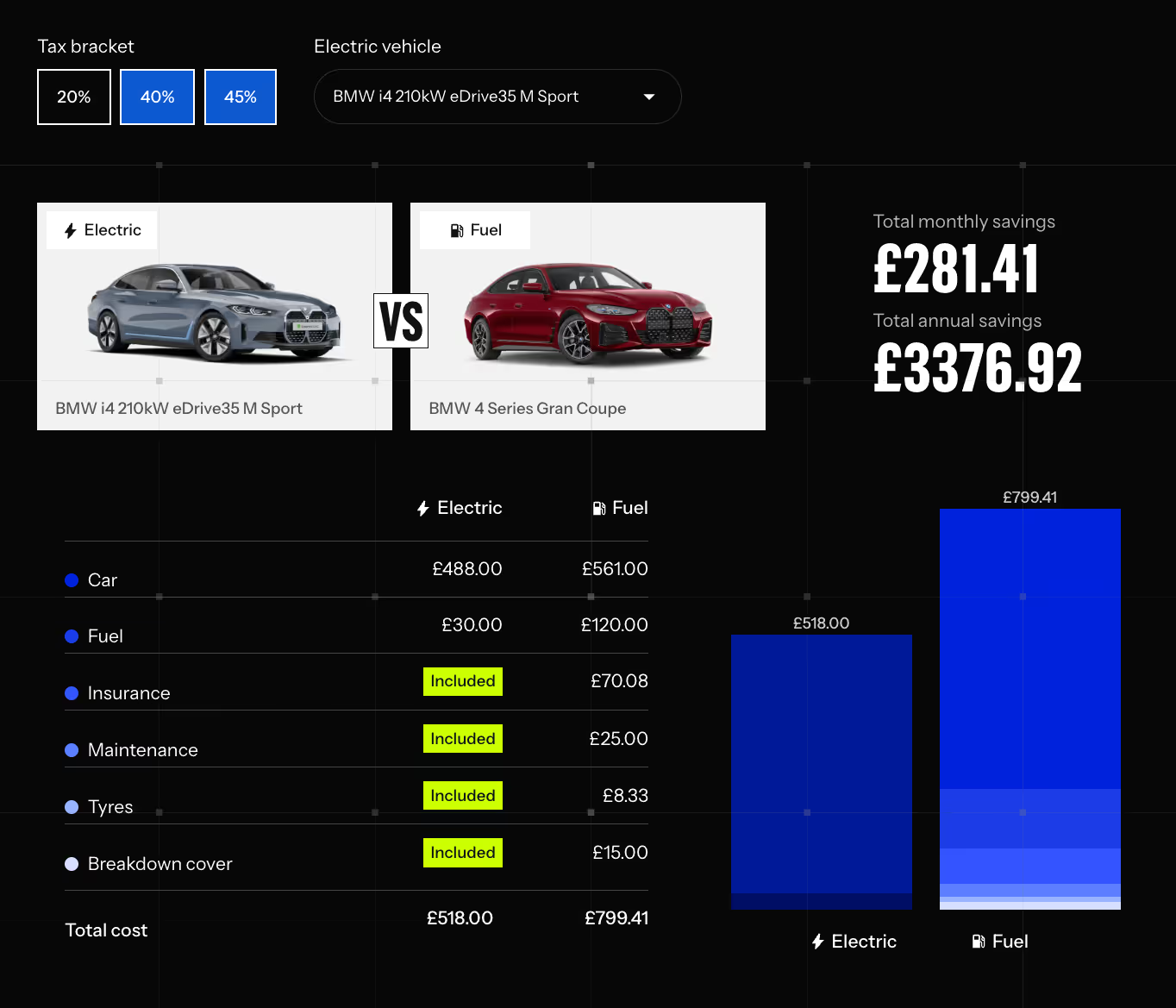

Comparing combustion car vs electric car (with an example)

Perhaps you like a particular car brand and want to see how it differs from electric to combustion, or you’re still unsure if you’d like to go with combustion or electric.

In that case, let’s compare a combustion car with an electric vehicle on a salary sacrifice scheme to get the complete picture of cost savings.

If you’d like to see how the numbers stack up for your own situation, whether that’s comparing an electric car to its petrol equivalent or testing different salary levels, try our EV salary sacrifice calculator.

It shows your estimated monthly cost and tax savings side by side, helping you work out what switching to electric could really save you.

Example of the fuel cost difference between a combustion car and an electric car

In general electric cars are cheaper to run than their petrol counterparts. An example calculated via nextgreencar using the example of a Vauxhall Corsa model with 5,000 annual miles shows the price of a petrol Corsa at £721 per year and the electric Corsa-e at £473 per year.

That's a 50% saving in your yearly vehicle fuel cost.

Want to learn the costs associated with running an EV? Check out our articles: How Much Is It to Charge an Electric Car: UK Guide 2025 and How Much to Install an EV Charger at Home: UK EV Charger Installation Costs Explained.

Want to see your exact saving?

These examples are based on typical scenarios. Your saving depends on your salary, tax bracket, and the car you choose. Use our salary sacrifice calculator to see your personalised monthly cost in under 60 seconds.

→ Try the Salary Sacrifice Calculator

Example of a driver order form with loveelectric

By now, you should have a better understanding of the pricing involved in a salary sacrifice scheme. As a bonus salary sacrifice electric car example, we’ll now look at what a typical driver order form looks like with loveelectric.

The process looks like the following:

- If you’re interested in signing up for loveelectric, send an enquiry and we’ll set you up.

- If you’re an employee, we’ll talk with your employer. As an employer, we’ll request some documents and you’ll need to complete credit checks with our partner car leasing companies.

- Sign a service agreement if you choose to continue (no cost).

- Get access to the live web application with real-time prices based on your insurance details and place your electric vehicle order.

- Employee picks the car (employer must agree) and receives the order form.

- Employees only start paying once the car arrives.

The order form will show you a recap of what you have ordered; like the make and model of the car, any extras and what protection you get.

We do not perform a credit check on employees, but for the insurance, we will require the driver's age, postcode and annual salary. You should check to ensure all the details are correct and notify the team of any discrepancies.

As an employee, you will see an overview of what’s included in your lease:

- How many miles per annum

- Lease term

- Maintenance & servicing

- Breakdown cover

- Early termination protection

- Fully comprehensive insurance: (Optional)

.avif)

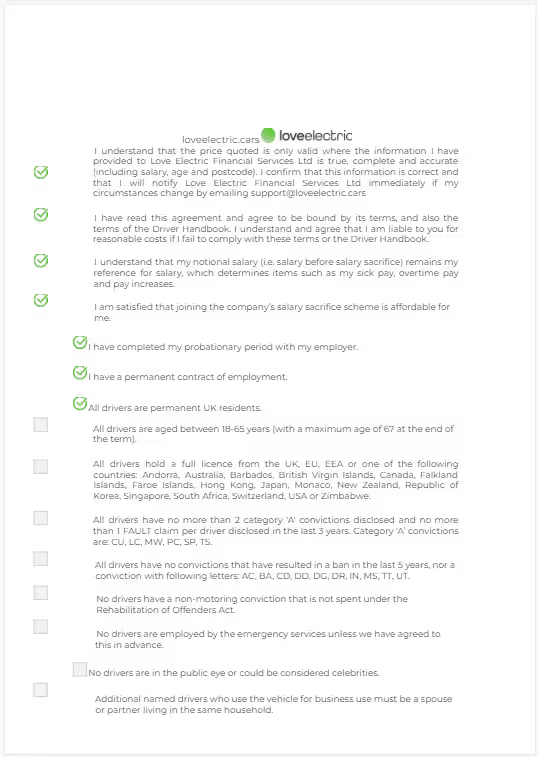

The order form also serves as a legal document for the driver, as you must agree to the terms and conditions laid out and sign it. Next, you’ll see a list of declarations followed by an eligibility section. A snapshot of this can be seen below.

Ready to loveelectric?

Whether your company already offers salary sacrifice or you’re starting from scratch, here’s the simplest way to move forward:

- My employer already offers the scheme → Get started as a driver: loveelectric for employees

- My employer doesn’t offer it yet → Share a quick note with HR: refer your company

- Not sure if your business is eligible? → Check in under a minute: eligibility checker

- Want to talk it through? → Speak to our team: send an enquiry

If the numbers in this guide looked good, the links above will get you from salary sacrifice car example to real-life EV.

Electric car salary sacrifice examples | FAQs

Hopefully, the above salary sacrifice car scheme examples have cleared up many of your queries. We’ve added a list of frequently asked questions that we hear a lot from our customers to explain further why we think salary sacrifice is so beneficial.

How much does EV salary sacrifice save?

You can save anywhere from 30 - 60% of the cost of a standard lease. You have the added benefit of monthly savings on the cost of fuel compared to a combustion car.

In this article, we have shown real-world examples of these savings.

Is salary sacrifice a better option than buying a car?

We believe it’s far better to salary sacrifice over buying an electric car. You'll typically have far higher monthly payments when buying a car through the three most common methods (PCP, Hire Purchase or bank loan). You’ll also miss out on the tax savings.

With a salary sacrifice scheme, you’ll have far more flexibility to upgrade to a brand new electric car every few years. With the rate at which technology for electric vehicles is increasing, it’s better to always have the most up-to-date version rather than being stuck with an old model you bought.

You’ll eventually have to sell that electric car if you buy it, which is already a headache in itself. Also, you’ll be dealing with the hassle of selling into an already further evolved marketplace. Most people won’t want to buy old technology.

With salary sacrifice, there is very little work to do. All your maintenance, servicing and insurance are already taken care of. At the end of your lease, you can seamlessly just lease again for a newer model with up-to-date batteries and a longer range.

Can you own the car through salary sacrifice?

No, with salary sacrifice you are leasing a car, not owning it, just like any other lease.

Some salary sacrifice providers will allow you to buy the car after your lease contract is over, but they won’t share the price until later on in your contract.

At loveelectric, you’ll lease the car and will only be able to buy the vehicle under extenuating circumstances - but this is not the norm. As we mentioned above, buying an electric car doesn’t always make sense since the technology is developing so rapidly.

If you’re deciding on whether to lease or buy your car, check out our article on leasing vs buying.

What are things to consider with salary sacrifice?

You will earn less over the year by taking the cost out of your gross salary. A lower salary could mean that you have less borrowing potential, which can be based on a multiple of your take-home pay. It’s worth considering this if you plan to take out a loan via a lender while leasing on salary sacrifice.

It’s also worth noting that not all salary sacrifice schemes are the same. In some cases, they have very different cost structures, hidden fees or poor customer service. Be sure to check out online reviews on sites such as Trustpilot.

Additionally, not all salary sacrifice schemes will include delivery of the vehicle to your home. With loveelectric, our prices always include delivery unless otherwise stipulated.