Employee tax benefits for EV schemes: How salary sacrifice with loveelectric saves you thousands

There aren’t many ways to save on tax that HMRC actually encourages. But EV salary sacrifice is one of them.

It’s a simple, government-backed benefit that lets employees pay for an electric car before tax, cutting both Income Tax and National Insurance in the process.

If you’re here wondering whether it’s worth signing up to the scheme or thinking about bringing it into your company as a benefit, this guide breaks down everything you need to know about the employee tax benefits for EV schemes.

We’ll also show example tax savings for every salary bracket with real cars you could get through the loveelectric salary sacrifice car scheme.

What are the tax benefits of an EV salary sacrifice scheme?

Getting access to a more affordable EV is enough of a win for most people, but there’s a lot more under the hood of an EV salary sacrifice scheme to get excited about.

From Income Tax and National Insurance savings to government-backed incentives that keep Benefit-in-Kind rates low, here’s how the tax benefits of an EV salary sacrifice scheme start working in your favour.

You pay from your gross salary, so you’re taxed on a smaller number

This is the foundation of every salary sacrifice scheme and the biggest reason it’s so tax efficient.

Instead of paying for your car from your take-home pay like you would with a personal lease, the cost is taken from your gross salary (the amount before Income Tax and National Insurance are applied).

That single change means you’re taxed on a smaller income, which instantly reduces both of those deductions. Here’s a simplified example from one of our drivers:

Before salary sacrifice, they earned £4,583 a month.

After tax and National Insurance, their take-home pay was £3,397.

Once they joined the scheme and sacrificed £475 of their monthly gross salary for an electric car, their taxable income dropped to £4,108.

And so, their Income Tax fell by £200 and National Insurance by £14, with only a small £21 Benefit-in-Kind charge added back. Their new net pay was £3,115. That’s a 41% saving on the car’s cost.

.avif)

Because your savings come from reduced tax and NI, the higher your tax band, the more you benefit. But even basic rate taxpayers can see hundreds of pounds saved every month compared to a standard lease.

📚You may also like: How Does Salary Sacrifice for Cars Work: A Guide to the EV Scheme and 7 Best Salary Sacrifice Car Scheme Providers Compared

EVs are treated differently by HMRC than other salary sacrifice schemes

Most benefits offered through salary sacrifice are taxed under strict rules called Optional Remuneration Arrangements (or OpRA for short). Normally, these rules limit how much tax advantage you can get when swapping part of your salary for a non-cash benefit.

Electric cars are the exception.

HMRC has specifically exempted zero-emission vehicles from those rules to encourage drivers and employers to make the switch.

Instead of being taxed on the salary you give up, you’re only taxed on the car’s Benefit-in-Kind (BiK) value, which for EVs is currently just 3% of the car’s list price.

That 3% BiK rate is one of the lowest you’ll find anywhere in the tax system.

It’s what makes EV salary sacrifice schemes so powerful compared to petrol or diesel alternatives, where BiK rates can easily exceed 25–30%. And because the government has confirmed that EV BiK rates will stay low for several years, your monthly payments stay predictable and the savings consistent

👀How that looks in practice

Let’s say you drive an electric car with a list price of £40,000.

Under the current 2% BiK rate, you’re taxed on just £800 of benefit value for the entire year.

If you’re a basic rate taxpayer (20%), that means an extra £160 in tax for the year — or around £13 per month.

Even for a higher-rate taxpayer at 40%, it’s just £320 a year, roughly £27 per month.

That’s the only tax you pay on the car itself, compared to the thousands you’d lose in Income Tax and National Insurance if you leased the same vehicle privately.

Important to know: the BiK rate is scheduled to rise gradually to 4% in 2026/27, and 5% in 2027/28. Even then, it will remain dramatically lower than the rates applied to petrol and diesel cars, keeping EV salary sacrifice one of the most tax-efficient ways to drive.

You can reclaim your Personal Allowance and avoid the 60% tax trap

If you earn over £100,000 a year, you’re likely familiar with the frustrating tax trap that kicks in once your income crosses that threshold.

For every £2 you earn above £100,000, your tax-free Personal Allowance (currently £12,570) reduces by £1. By the time you reach £125,140, it disappears completely.

That means part of your income between £100,000 and £125,140 is effectively taxed at 60%, one of the steepest marginal rates anywhere in the UK tax system.

Salary sacrifice can pull you out of that trap. By sacrificing part of your gross salary for an electric car, your taxable income falls. If that brings your earnings back under £100,000, you reclaim your Personal Allowance and immediately reduce your effective tax rate.

For example, if you earn £105,000 and sacrifice £6,000 a year through an EV salary sacrifice scheme, your taxable income drops to £99,000.

You not only regain your full £12,570 Personal Allowance but also save thousands in Income Tax and National Insurance. All while driving a brand-new electric car.

This is one of the biggest untapped benefits of salary sacrifice for higher earners. It turns what would normally be lost to tax into a tangible, everyday upgrade.

You could regain access to family benefits like free childcare

If your income pushes you just above £100,000, you can also lose access to valuable family benefits.

One of the most common is the 30 hours of free childcare offered by the UK government, which is only available to households where each parent earns under £100,000.

By using salary sacrifice to bring your taxable income below that threshold, you could regain eligibility for those benefits. That means an electric car through your employer could effectively pay for itself, not just through lower tax and running costs, but through the family savings it unlocks.

For higher-earning parents, this combination of reclaimed childcare support and lower Income Tax makes EV salary sacrifice one of the most financially rewarding employee benefits available.

All your running costs are covered in a tax-efficient way

Another hidden advantage of salary sacrifice is that it doesn’t just make the car itself cheaper, it wraps most of your ongoing motoring costs into that same pre-tax payment.

With a Loveelectric lease, your monthly amount typically includes:

- Fully comprehensive insurance

- Servicing, maintenance, and tyres

- Breakdown cover and accident management

Because all of these are bundled into the single amount you sacrifice from your gross salary, they’re effectively paid for before tax. That means you’re saving on the everyday costs of running a car, not just the lease itself.

In contrast, when you lease or buy a car privately, those same expenses are covered from your take-home pay, after Income Tax and National Insurance have already been deducted.

Salary sacrifice turns all those outgoings into tax-efficient essentials, which is one of the reasons drivers regularly see 30–60% savings compared to a personal lease.

📚You may also like: Is EV salary sacrifice worth it? Car scheme pros and cons

It’s HMRC-backed, not a tax loophole

One of the biggest misconceptions about salary sacrifice is that it’s some kind of clever tax dodge. It’s not.

It’s actually the opposite. EV salary sacrifice is a government-approved incentive designed to make low-emission driving more accessible.

HMRC specifically exempts electric vehicles from the usual salary sacrifice restrictions under the Optional Remuneration Arrangements (OpRA) rules. That means the tax savings you make are fully compliant and intentionally built into the system to encourage greener transport.

So, EV salary sacrifice isn’t bending the rules, it’s taking advantage of them exactly as the government intended.

And because the Benefit-in-Kind rates for EVs have already been confirmed for the next few years, your tax position stays stable and predictable long after you’ve driven the car off the lot.

Every tax benefit we shared with you so far is one you can trust. There’s no risk and no repercussions. That’s a pretty good benefit in and of itself.

So, how much tax can you save? (with examples)

Exactly how much you’ll save through salary sacrifice depends on two things:

- your income tax band

- the value of the car you choose

The higher your tax rate, the more each pound you sacrifice works in your favour. But even at the basic rate, the savings add up fast once you factor in lower running costs and the small Benefit-in-Kind charge.

Let’s look at a few simple examples based on real loveelectric data.

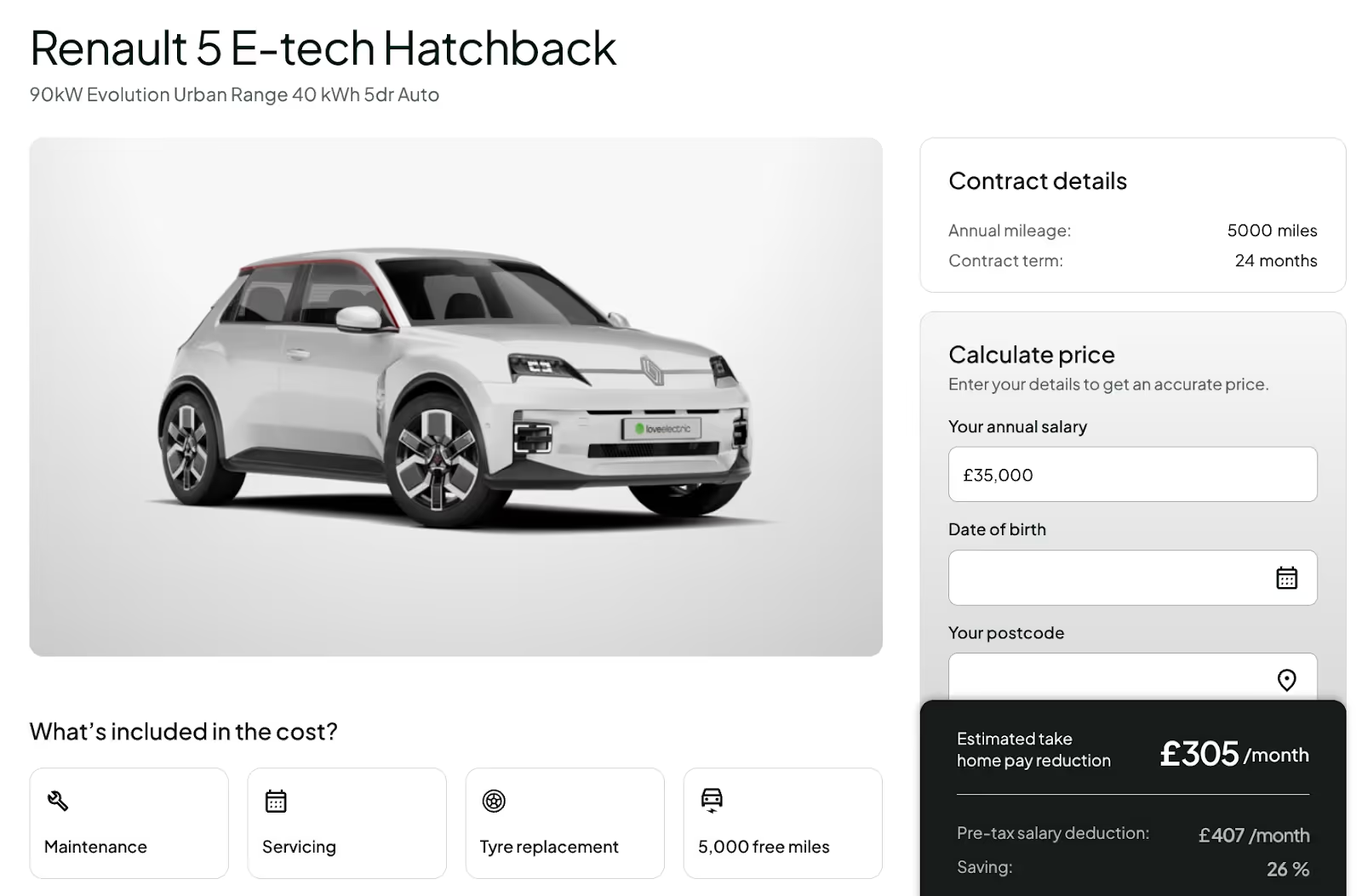

Example 1: Basic rate taxpayer (20%)

Salary: £35,000

Car: Renault 5 E-Tech Hatchback

Gross monthly lease: £407

Estimated take-home pay reduction: £305

Net saving: around 25 %

A driver earning around £35,000 could get a brand-new Renault 5 E-Tech Hatchback through salary sacrifice for £407 a month before tax, with their take-home pay only reduced by about £305 per month once Income Tax and National Insurance savings are applied.

That difference, just over £100 every month, comes entirely from the tax advantages of salary sacrifice.

Even before factoring in lower running costs (like charging instead of petrol, or fewer maintenance expenses), this driver is already saving significantly compared with a private lease.

Something to know: Most providers limit their schemes to higher earners, but Loveelectric’s setup is more inclusive. We can support employees earning as little as £27,000 a year, as long as the lease doesn’t take their income below the National Minimum Wage threshold. This is in large part possible because we offer the loveelectric’s Reloved® range. These are high-quality used EVs that come fully insured, maintained, and protected under the same salary sacrifice benefits as new cars.

For many drivers, that combination of lower monthly cost and full tax efficiency is what turns an electric car from a “someday” goal into a practical, everyday option.

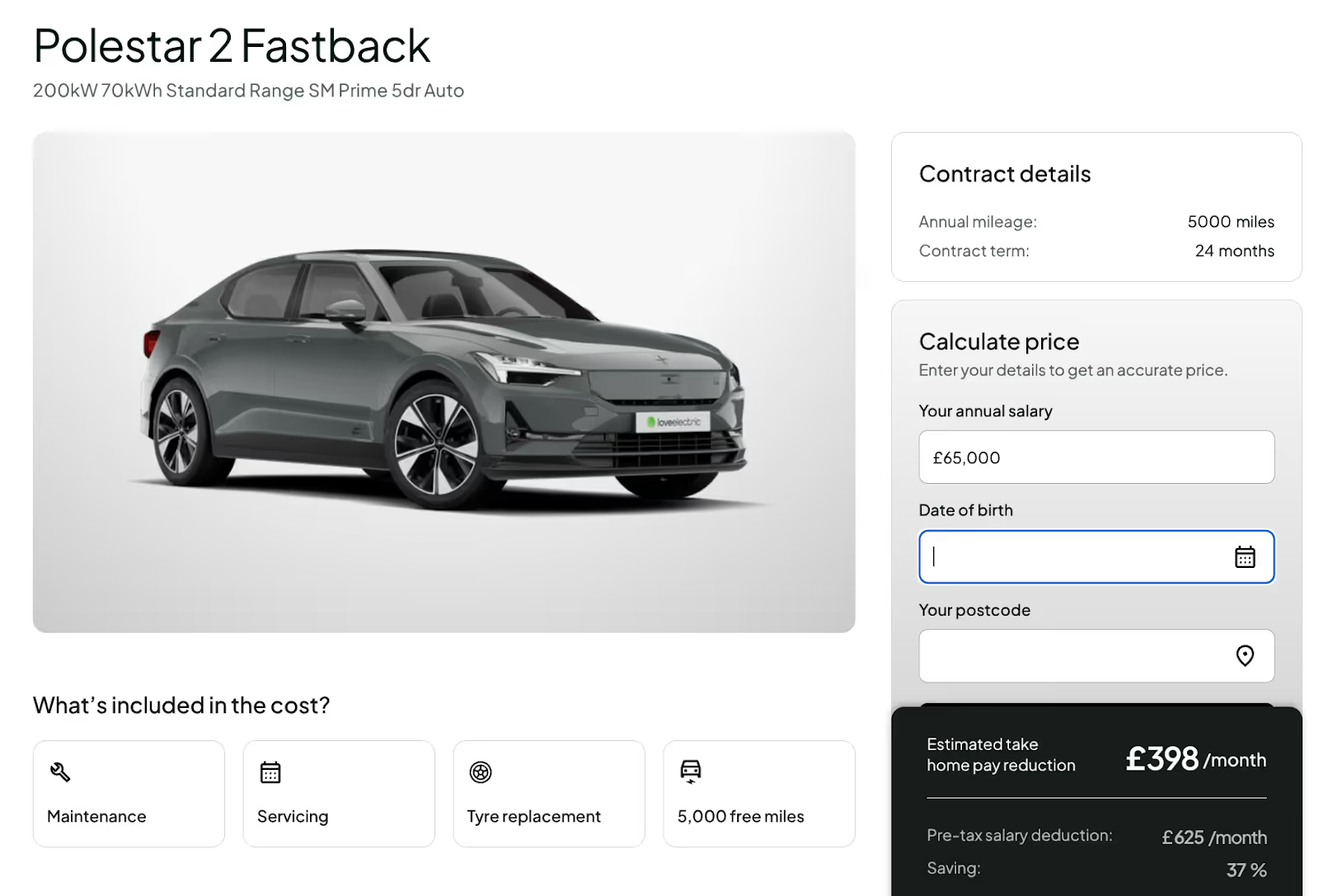

Example 2: Higher-rate taxpayer (40%)

Salary: £65,000

Car: Polestar 2 Fastback

Gross monthly lease: £625

Estimated take-home pay reduction: £398

Net saving: 37%

For someone earning around £65,000, choosing a Polestar 2 through salary sacrifice means sacrificing £625 of gross salary each month.

After Income Tax and National Insurance savings, their take-home pay only falls by £398, a saving of roughly £227 per month compared with leasing privately.

That’s the power of paying from pre-tax income. In practice, it makes a premium EV like the Polestar 2 as affordable as a mid-range petrol hatchback. And with Benefit-in-Kind rates for EVs staying low for the next few years, those savings are consistent and easy to plan for.

Example 3: Additional-rate taxpayer (45%)

Salary: £110,000

Car: Tesla Model Y Rear-Wheel Drive

Gross monthly lease: £819

Estimated take-home pay reduction: £301

Net saving: 64 %

For someone earning around £110,000, choosing a Tesla Model Y through salary sacrifice means sacrificing £819 of gross salary each month.

After Income Tax and National Insurance savings are applied, their take-home pay only falls by £301.

That’s a saving of more than £500 every month compared with leasing the same car privately, over £18,000 across a three-year lease. Because their taxable income also drops below £100,000, this driver could reclaim their full Personal Allowance and regain access to benefits such as 30 hours of free childcare.

For high earners, that combination of meaningful tax recovery and premium EV access is hard to beat.

How your payslip changes

One of the most common questions employees have about salary sacrifice is, “What will this look like on my payslip?” The answer is: surprisingly simple.

When you get an electric car through salary sacrifice, your gross salary (the amount before tax and National Insurance) is reduced by the cost of the car. You’ll then see your Income Tax and NI deductions fall in line with your new, lower taxable income. The car lease itself appears as a salary sacrifice deduction, usually labelled something like EV Lease or Salary Sacrifice Car.

Here’s a simplified example to show what that looks like in practice:

.avif)

The key thing to remember is that your take-home pay drops by less than the car’s cost, because you’re paying from pre-tax income.

Everything is handled automatically through payroll, so there’s no manual claiming, no separate payments, and no paperwork at the end of the month.

Are there any tax downsides to watch out for?

Salary sacrifice is one of the most tax-efficient ways to drive an EV, but there are a few things to be aware of before signing up. None of them are deal-breakers, you just need to understand how they work.

1. Your gross salary is reduced

Because salary sacrifice lowers your gross pay, it can affect calculations that use your pre-tax income. For example, mortgage applications or pension contributions.

The impact is usually small, but it’s worth checking if you’re planning a big financial change, like applying for a mortgage or remortgaging.

2. Early termination costs (if you leave your job)

If you leave your employer during your lease period, most providers charge early termination fees.

However, with loveelectric, that risk is removed. Our Zero Risk Guarantee protects both you and your employer from early exit costs in situations such as resignation, redundancy, illness, or parental leave.

It means you can enjoy all the tax savings of salary sacrifice without worrying about being tied in if your circumstances change.

loveelectric: Your tax-efficient route to an EV

Salary sacrifice is one of the most accessible ways to make the switch to electric driving and with loveelectric, it’s built to work for everyone.

We’re a technology-driven platform, not a traditional leasing company. That means we partner with the UK’s largest leasing providers to secure the best possible prices every single day, often up to 60% cheaper than leasing privately.

Every car on our platform is part of a government-backed, HMRC-approved scheme that makes EVs genuinely affordable, whether you’re an employee or an employer.

Already have access to loveelectric?

Explore the range and see how much you could save. → Browse cars

Wish your company offered salary sacrifice?

Be the one who brings it to your team. → Refer your company

Want to offer a cost-neutral benefit employees will love?

Offer one of the UK’s most cost-neutral, sustainable employee benefits and make electric cars attainable for your whole team. → Check your company’s eligibility

Or speak directly with our team to see how we can help you get started.

Loveelectric makes it easy to turn tax efficiency into impact, for your finances, your business, and the planet.

_cropped_processed_by_imagy%20(2).avif)