What Is a Reasonable Car Allowance? Average Offer in UK

Car allowances are one of those benefits that sound simple, until you try to decide what’s reasonable and actually covers the ever changing costs of running a car.

This guide breaks down the latest average car allowance figures across the UK, what affects those numbers, and how to tell if your allowance still makes sense today. We’ll also look at EV salary sacrifice, a tax-efficient, greener alternative that more companies are offering in place of traditional cash allowances.

What is a reasonable car allowance?

Any reasonable car allowance should cover the cost of using your own car for work. That’s things like fuel, insurance, and maintenance.

Some roles expect a newer car or higher mileage, while others involve only occasional travel. Either way, your allowance should make it easy to keep a reliable car on the road without eating into your pay packet.

Average car allowance in the UK (2025 figures)

As car allowances are a benefit, and benefits are designed to entice and reward talent, companies often look to each other to decide what’s reasonable to offer.

For employees, it’s just as useful to know the going rate. Checking the averages is a simple way to sense-check whether what you’re getting is fair.

Across the UK, most company car allowances fall somewhere between £3,600 and £10,000 a year. It all depends on how often a car is needed for work and the level of responsibility attached to the role.

Research from Aaron Wallis Sales Recruitment suggests that:

- Field and area sales roles tend to sit at the lower end of the scale, around £3,700–£4,500 a year, since these roles often come with mileage reimbursements on top.

- Managers and department leads usually see £5,000–£7,000, reflecting higher travel expectations and a need for a newer, more presentable car.

- Executives and directors can expect anywhere from £8,000–£13,000, especially in organisations where a car is seen as part of the overall status package.

The trend in 2025 is upwards. With rising fuel, insurance, and servicing costs, more employers are increasing allowances or revisiting their car policies altogether.

Whether you’re setting a policy or assessing your own package, these averages give a useful reference point for what’s typical, but what’s reasonable still depends on how much you drive, what your role demands, where you’re located and several other factors.

What factors decide a reasonable car allowance?

There’s no universal rulebook for what makes a “reasonable” car allowance. But there are factors that can help you reach figures that are fair and which reflect what it costs to stay on the road in 2025.

Here’s what influences your car allowance figures:

Role and seniority

Allowances should scale with responsibility, especially when those responsibilities require more time on the road. A regional manager visiting multiple sites every week has completely different needs from an office-based colleague who drives once a month.

Mileage expectations

The more an employee drives, the faster their car depreciates. High-mileage roles rack up wear and tear that a £4,000 annual allowance can’t realistically cover.

Employers who want to stay competitive are starting to use mileage-based tiers or hybrid models that blend allowance with mileage reimbursement.

Industry norms

Sales, property, and logistics roles typically command higher car allowances because a car is integral to the job. HR and professional services tend to sit lower. Knowing where your sector sits helps employers stay competitive and helps employees spot when their package is behind the curve.

Region and cost of living

Running a car in London or the South East costs more. That’s just reality. Fuel, insurance, and parking all add up. So if you have employees in more expensive areas, they’ll need a larger car allowance for it to feel like a benefit and not a point of contention.

Fuel type and sustainability goals

As more companies set net-zero targets, car allowances are quietly becoming part of the sustainability conversation. Some now offer higher allowances or EV-friendly schemes to encourage greener driving. Others are switching entirely to EV salary sacrifice car schemes, a move that’s tax-efficient and aligned with ESG goals.

Not sure how salary sacrifice works? Check out our guide: How Does Salary Sacrifice for Cars Work: A Guide to the EV Scheme

Insurance and maintenance costs

Insurance and servicing costs have jumped significantly in recent years, with claim costs up by around 30-35% since 2019. Servicing costs are up too.

So, any employer still using pre-2020 allowance figures is almost certainly underpaying relative to current market conditions.

Competitiveness and retention

The better your benefits package, the better chance you have at pulling top talent into your organization. If your car allowance figure falls short of your competitors or even just other employers, you could be losing out.

Is your car allowance enough? What it should cover

Once you know what influences your company’s car allowance, the next question is simpler. Does yours actually cover what it’s meant to?

Here’s a quick check to see whether your allowance still matches reality in 2025/2026:

- Fuel and mileage: Can you fill up for work trips without reaching into your own pocket?

- Insurance: Does your policy include business use and does your allowance reflect the extra premium that brings?

- Servicing and MOTs: Are routine costs covered, or are you spreading them out of pocket through the year?

- Depreciation: Are you accounting for the wear-and-tear value your car loses from work travel?

- Professional image: If your role involves client visits, can you afford to keep your car presentable and reliable?

If you’re falling short on two or more of these, your allowance probably isn’t keeping pace with real-world costs. A car allowance should make driving for work feel like part of the job, not part of your personal spending. If it doesn’t, it’s worth raising the question.

How to calculate whether your company car allowance is fair

Whether you’re setting allowances or receiving one, a quick calculation can show if the figure really adds up.

Start with your annual business mileage, then multiply it by the average cost per mile for your car type. For petrol or diesel cars, that’s usually around 45–50p per mile. For electric cars, closer to 20–25p. (You can find updated HMRC advisory rates here).

Then factor in the fixed annual costs that aren’t mileage-dependent:

- Insurance (including business use)

- Servicing, MOTs, and tyres

- Depreciation — roughly 15–25% of your car’s value each year if you drive regularly for work

Once you’ve added those together, compare the total to your gross annual car allowance.

If your allowance comfortably covers those costs (even after tax), you’re in the right range. If not, it’s likely outdated, especially given 2025’s higher repair and insurance costs.

For example:

- 10,000 work miles × 45p = £4,500 in running costs

- Add £1,000 insurance and £1,000 in depreciation = £6,500 total

- A £5,000 annual allowance wouldn’t quite cover that.

For HR teams, this calculation helps keep packages competitive. For employees, it’s a quick reality check to bring into a pay review conversation. Either way, the numbers don’t lie. They’re a good starting point for a fairer, more transparent approach to car allowances.

But they are a starting point. Because those other factors we mentioned might add to the allowance costs, especially for higher earners and senior roles in your business.

Salary sacrifice: The tax-efficient alternative to car allowances

As car running costs rise and sustainability moves up the agenda, many UK companies are rethinking how they help employees get behind the wheel.

For a growing number, the answer isn’t a higher cash allowance, it’s salary sacrifice.

Employees exchange part of their gross salary for a leased car, typically an EV, with payments taken directly through payroll before tax and National Insurance. That structure means both employees and employers save money, while supporting a shift to cleaner, lower-emission vehicles.

For employees, the benefits of salary sacrifice stack up fast:

- Tax and NI savings — payments are deducted before tax, making the car far cheaper than buying or leasing privately.

- Lower running costs — electricity is still far cheaper than petrol, and EVs typically need much less maintenance.

- All-in-one simplicity — the lease usually includes insurance, maintenance, breakdown cover, and road tax, so there are no surprise costs.

Employers benefit too:

- Greener company image — offering EVs through salary sacrifice supports sustainability goals and cuts fleet emissions.

- Better talent attraction and retention — it’s a high-value perk that feels modern without increasing base salaries.

- Cost-neutral setup — most schemes run through providers like loveelectric, meaning there’s minimal admin or financial risk for the business.

📚Read more about how companies financially benefit from salary sacrifice.

Of course, salary sacrifice is different to a traditional car allowance.

With salary sacrifice, the employer is responsible for the lease of the vehicle but the employee is the one paying for it out of their salary. While a car allowance goes toward the costs of a vehicle the employee buys on their own, after tax.

With a salary sacrifice provider like loveelectric, your employees can save up to 60% on the EV of their dreams. And because we offer new and used vehicles, more of your employees can take advantage of the benefit than with other salsac companies.

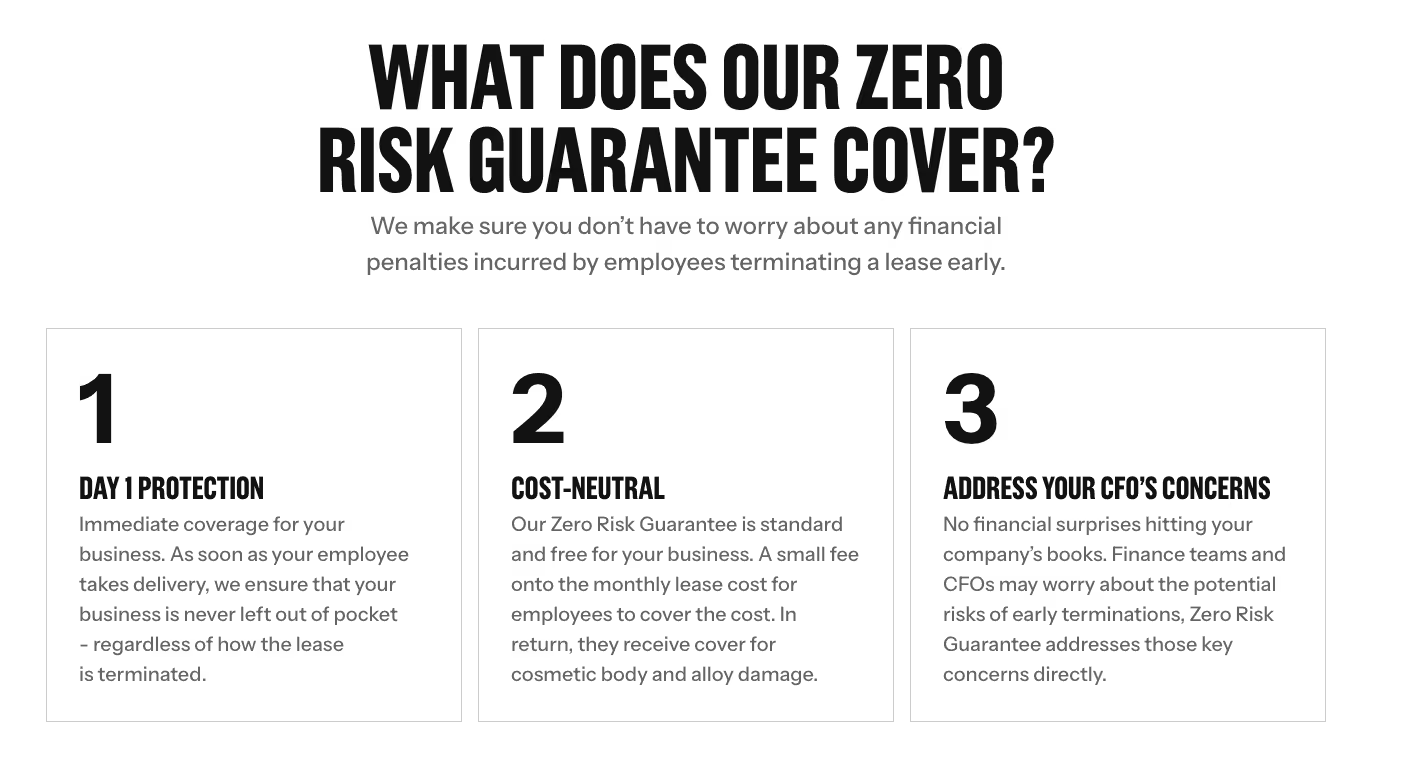

Plus, with our Zero Risk Guarantee the scheme can be run without putting your business in financial risk.

See what cars are available through the loveelectric, check your company’s eligibility to run the scheme, or enquire with us today to get this benefit set up in just a few weeks.

And if you’re an employee and wish your company would bring on the EV salsac scheme, refer them to us today.

Reasonable Car Allowance FAQs

Do you have to spend your car allowance on a car?

No, there’s no legal requirement to spend your car allowance on a vehicle. Once it’s paid as part of your salary, it’s treated like income, meaning you can use it however you choose.

Most employers expect you to keep a reliable car for work use, but how you fund it is up to you.

Is car allowance taxed in the UK?

Yes. Car allowances are paid as cash, so they’re subject to Income Tax and National Insurance just like regular salary. That means the amount you receive after deductions will be lower than the figure in your contract.

Is a car allowance better than a company car?

It depends on your driving habits and tax bracket. A company car can offer convenience, but you’ll pay Benefit-in-Kind (BiK) tax on it, especially high for petrol and diesel cars. An allowance gives flexibility but may not stretch as far once taxed.

What’s the difference between a car allowance and salary sacrifice?

A car allowance is a cash payment and therefore taxed as income. You can use it to buy, lease, or maintain a car. A salary sacrifice scheme works differently.

You exchange part of your gross salary (before tax) for a leased car, usually an EV, cutting your tax bill and lowering overall costs. Your company is the one leasing the vehicle so they’ll be the ones going through a soft credit check. That’s not the case for a car allowance.

_cropped_processed_by_imagy%20(2).avif)