Does Salary Sacrifice Affect Mortgage Applications? Our Take

.avif)

Short answer? Yes, most salary sacrifice schemes do affect mortgage applications. But don’t sack off the idea of salary sacrifice just yet or panic if you have a scheme and are in need of a mortgage.

You need more than a yes or no answer, you need to understand how, why, and what you can do about the impact it has. So, let’s rewind a bit.

Salary sacrifice can sound like free money. You swap a slice of your salary for a shiny new benefit, often an electric car, and in return pay less tax and National Insurance.

But when it comes to mortgages, things get a little more complicated. Some lenders see the reduced salary and assume you can borrow less. Others look more deeply, especially if you can prove your pre-sacrifice income or show that the benefit (like your EV lease) actually saves you money elsewhere.

In this guide, we’ll unpack how salary sacrifice really plays into mortgage decisions, what lenders look for, what you can do about it, and whether it’s ever worth holding off on the scheme. By the end, you’ll have the full picture, not just the TikTok take.

Disclaimer: loveelectric does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Please seek independent financial advice.

Types of salary sacrifice and their mortgage impact

Before we get into how lenders treat salary sacrifice, it helps to know that not all schemes are treated the same by mortgage brokers. Some have next to no impact on your mortgage application, while others can make lenders pause for a closer look.

Here’s a quick run-through of how different salary sacrifice schemes tend to show up in mortgage decisions:

If EV salary sacrifice is the scheme your company offers and one you want to take advantage of, don’t worry too much. With clear documentation and the right provider, most lenders are perfectly comfortable with these arrangements.

There’s real-world proof available. On a Reddit thread, users shared their experiences getting mortgages with salary sacrifice:

Choosing the best salary sacrifice car scheme helps lenders see the structure and stability behind your setup.

If you’re new to the idea, here’s exactly how to get a car on salary sacrifice and what the process looks like for employees. Or, for a refresher, learn how salary sacrifice works to see why it’s such an effective way to drive electric while saving on tax.

Why salary sacrifice affects your mortgage application

When you join a salary sacrifice scheme, your taxable salary goes down. Great news for your take-home pay and tax savings, but not always great news when a lender looks at your income.

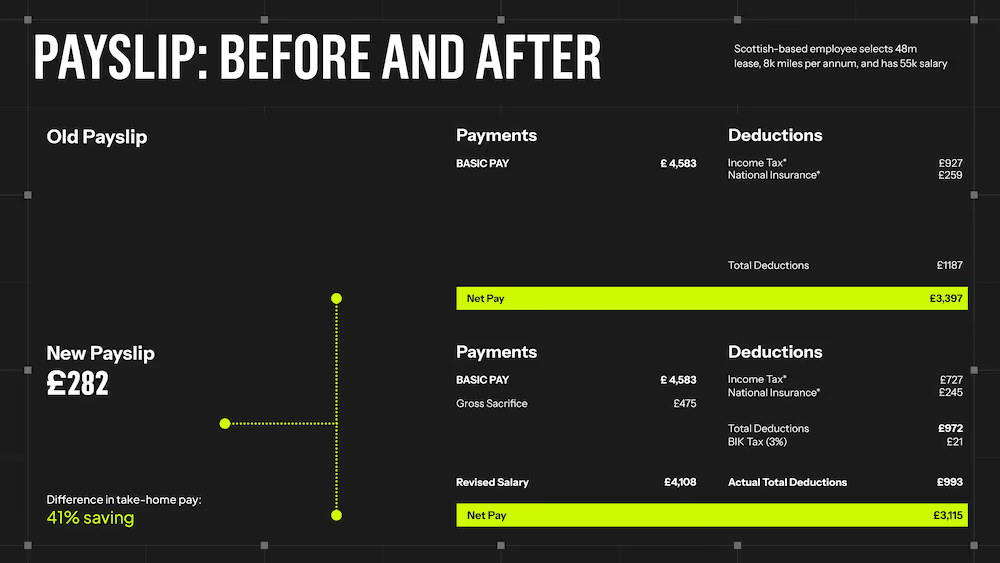

That’s because most mortgage lenders base their affordability calculations on the figure shown on your payslip, and that number is your post-sacrifice salary. Here’s an example:

So, if you’ve reduced your gross salary to lease an electric car, a lender may see you as earning less, even though your actual financial position might not have changed much.

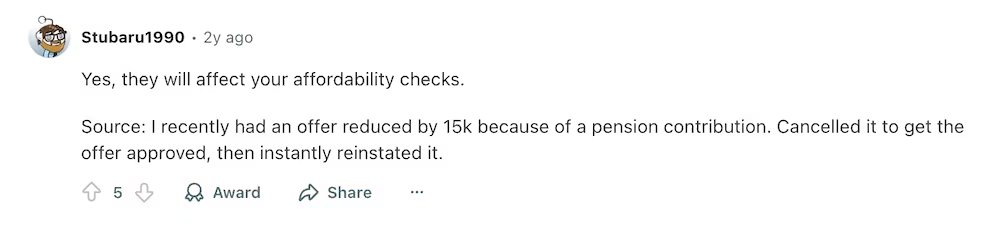

On that Reddit thread we mentioned earlier another user commented:

That said, not every lender treats it the same way. Some will consider your pre-sacrifice salary if you can show evidence like an employer letter or past payslips.

Salary sacrifice and mortgage affordability checks: How much can it reduce your borrowing?

Most UK lenders base mortgage affordability on around 4 to 4.5 times your annual salary . Some specialist or higher-income applicants may stretch to 5 or even 6 times salary, but those cases are the exception rather than the rule.

So, even a small reduction in your gross pay can shift the maths.

For example, if your salary drops from £60,000 to £55,000 after starting an EV salary sacrifice, a lender using a 4.5× multiple might reduce your maximum borrowing from £270,000 to £247,500. That’s a difference of around £22,500.

It’s not dramatic, but it’s worth knowing about if you’re planning to buy soon.

Curious how salary sacrifice affects your take-home pay across different incomes or what kinds of electric cars are available within each bracket, check out our guide: 9 Salary Sacrifice Electric Car Examples.

How lenders come up with a mortgage offer when salary sacrifice is in play

Every mortgage offer starts with one question: how much can you realistically afford?

To answer that, lenders look closely at how your income is structured. That’s where salary sacrifice can raise a few eyebrows.

Here’s how the process typically works behind the scenes.

They start by assessing your income source: Gross vs. post-sacrifice salary

Most lenders begin with what’s on your payslip. If your gross salary has been reduced through salary sacrifice, that lower figure is what they’ll usually plug into their affordability calculations.

However, some lenders, especially those used to working with public-sector or larger employers, are open to considering your pre-sacrifice salary, provided you can back it up with payslips or a letter from HR confirming your contractual pay.

They look at how permanent the sacrifice is

Flexibility makes a big difference. If your salary sacrifice is temporary or reversible, like many EV or pension schemes, lenders are more likely to treat your original salary as your true income.

If it’s fixed for a set term and can’t be changed until the contract ends, they’ll often use the reduced figure instead, simply to stay on the cautious side.

They compare your payslips and employment contract to verify affordability

Underwriters will want to see evidence that your income is stable and ongoing. Expect to provide:

- Your last three months of payslips

- A recent P60

- Your employment contract or an employer letter confirming your pre-sacrifice salary

They apply internal lending policies to decide how much income to count

Finally, each lender uses its own criteria to determine what percentage of your income counts toward affordability.

For example, some banks may accept 100% of your pre-sacrifice income if it’s proven reversible, while others might apply a more conservative approach.

Is salary sacrifice worth it if you’re planning a mortgage?

If a salary sacrifice can make lenders see you as earning less, is it worth holding off until after you’ve bought your home? That’s really what’s at the heart of this topic.

The answer is that it depends on timing and priorities.

In the short term, a salary sacrifice might reduce how much you can borrow, but not by a huge amount. In the long run, the tax and National Insurance savings (plus the chance to drive a brand-new EV) usually outweigh that small difference.

Here’s how to think about it:

If you’d like to weigh up the pros and cons in more detail, check out our guide on Is EV Salary Sacrifice Worth It?. It breaks down real examples of when the savings make sense, even if you’re thinking about buying a home later on.

How to get a mortgage while using a salary sacrifice scheme

You don’t need to choose between your dream EV and your dream home, you just need to approach your mortgage application with a little extra prep.

Here’s how to make it smooth sailing.

Step 1: Talk to a broker familiar with salary sacrifice

Not every lender interprets salary sacrifice the same way, so having a broker who “gets it” can make all the difference.

They’ll know which banks and building societies are flexible about EV or pension sacrifice schemes and which aren’t worth applying to.

A good broker can also explain the arrangement in the lender notes, highlighting that your car benefit actually saves you money each month through lower fuel, insurance, and maintenance costs.

Here’s what we’d do: Ask your broker if they’ve placed cases involving salary sacrifice before, especially for EVs. That experience can shave days off the approval process.

Step 2: Gather your documentation

Transparency is your best friend here. Lenders want to see what you earn now and what you could earn if you reversed your salary sacrifice.

That means having:

- Three months of payslips (to show consistency)

- A P60 or most recent tax statement (for annual totals)

- An employer letter confirming your contractual salary before sacrifice and stating whether the benefit is flexible or fixed

The clearer your evidence, the more likely a lender is to count your pre-sacrifice salary in place of the reduced figure on your payslip.

Step 3: Check your affordability ratios and credit health

Even if your declared income dips slightly, lenders assess your whole financial picture.

Keeping your credit utilisation low, loan repayments on time, and monthly outgoings predictable shows strong financial management. And that’s something lenders rate highly.

So don’t go crazy with credit in the weeks and months leading up to your mortgage.

If your debt-to-income ratio still looks healthy after salary sacrifice, that usually outweighs the headline salary change.

OR: Consider pausing sacrifice temporarily if applying soon

If you’ve done the maths and found that salary sacrifice trims your borrowing power a little too much, it can make sense to pause or delay joining the scheme until after your mortgage is approved.

That way, your payslips reflect your full salary during the lender’s affordability checks, giving you the best chance of securing the amount you need.

Once your mortgage offer is locked in, you can reinstate your salary sacrifice and start enjoying the tax savings (and the EV).

If you’re unsure whether pausing is possible, check with your HR or scheme provider because some may allow temporary adjustments.

FAQs: Salary sacrifice and mortgages

Which lenders accept salary sacrifice income in full?

It varies. Many mainstream lenders will consider your full income if you can show the salary reduction is voluntary and can be reversed.

Others may take a more conservative approach, basing affordability on your reduced salary.

This is where a broker familiar with salary sacrifice schemes can really help, they’ll know which lenders to prioritise.

You honestly won’t know until you speak to a broker or lender properly because mortgages are offered on a case by case basis.

Does salary sacrifice affect remortgaging later?

It can, but typically only in the same small way. When you remortgage, the lender will re-check your income, so the same rules apply: if your salary sacrifice reduces your taxable pay, it may slightly limit how much you can borrow.

As long as your payments are consistent and your credit record is strong, most people find remortgaging while on salary sacrifice straightforward.